Mass Affluent Customer Experience

Design strategy for PNC's Retail Banking group.

PROJECT DESCRIPTION | This experience design project was completed in 2016 for PNC's Retail Banking Group. The strategic intent for the project was to identify ways in which PNC could "grow share of wallet" with Mass Affluent customers by enhancing the customer experience at one or more key interaction points. The work included extensive consumer research, market research, workshop facilitation with line of business teams, and proof of concept development. Key deliverables for this project were synthesized research findings, customer personas, journey maps, and a white paper and a presentation developed for executive leadership.

ROLE | Design Strategist + Researcher

PROCESS |

For this project we decided to adopt the following working model. Though fairly common in the design community, it was new to the bank. This required us to educate the line of busness teams and sponsors along the way.

The project was completed with a team of three people over the course of nine months and was sponsored by the head of PNC's Retail Banking group.

PROJECT KICK-OFF | Scoping the project / Process employed / Customer Segment Overview

We kicked off the project with a day-long work session with various line of business partners and leadership. The session was focused on scoping the project, refining the project prompt, mapping out business needs, and understanding the customer segment. Through the session we were able to establish:

Current state Mass Affluent customer journey map

Hopes, Fears, Realities Matrix

Initial Hypotheses

Research Criteria

Breakdown of the customer segment

Gaps in PNC products/services

RESEARCH APPROACH | Focus areas / Participant Recruitment / Research Protocols + Tools

Research Focus Areas :

Better understand the mass affluent audience on a deeper, more meaningful level in terms of behavior, perceptions, attitudes and motivations.

Uncover opportunity areas to improve, change and enhance customer experience that will help to grow share of wallet with existing PNC financial products.

Understand the expectations that mass affluent customers have of their financial institution (What role do mass affluent customers want their financial institution to play and how do they want to be treated?)

Understand the triggers/threshold/levers to motivate a MA customer to change or consolidate Financial institutions for banking and/or investing.

Participant Recruitment:

Greater Washington Area: 20 Participants Total

12 participants in 28-45 age range with HHI $175K+ Investable assets $100K+

8 participants in 46-60 age range with HHI $175K+Investable assets $250K+

Pittsburgh: 22 Participants Total

6 participants in 28-35 age range with $125K+ in HHI

10 participants in 36-49 age range with $125K+ in HHI and $50K in investable assets

6 participants in 50-60 age range with $125K+ in HHI or $100K in investable assets

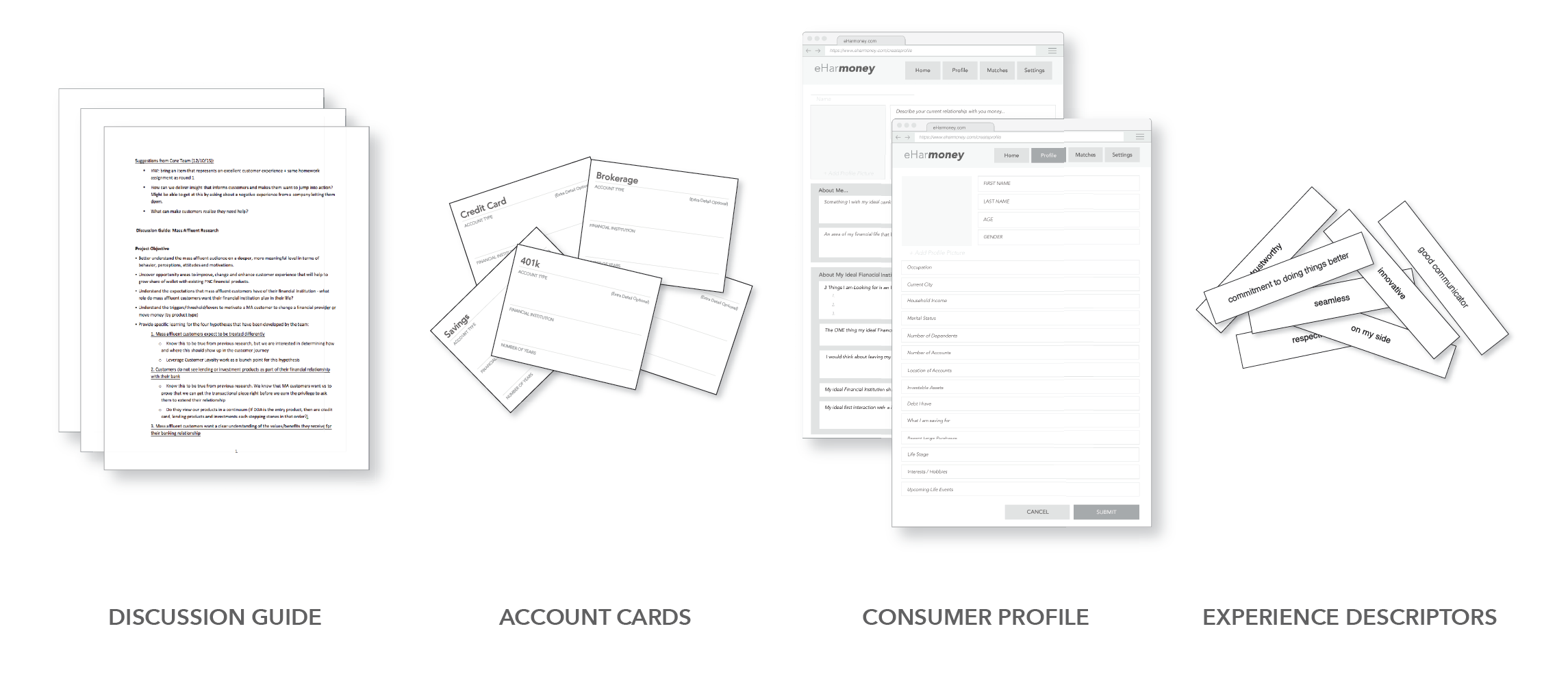

Research Protocol:

Each participant was scheduled for an hour-long in-person session. The session was broken into three phases, each based around an activity.

Activity One: Creation of "Account Cards" that represent each financial product the participant owns. This allowed for us to make the detailed and complex information regarding the participant's financial structure and both tangible and interactive.

Activity Two: Mapping of "Account Cards" using a matrix to understand the use of each financial product, reason for opening, and unmet needs.

Activity Three: Understanding Emotional Relationship with Finances - due to the abstractness of this conversation we used a online dating-style profile and experience descriptor cards as aides.

RESEARCH SYNTHESIS | Story Sharing / Theme Development

Story Sharing:

As we finished the customer interviews, we hung up images from the interviews and the materials created during the interviews as reference points for the Line of Business teams. Each member of the Core Team was given assigned transcripts to read and highlight. We then held a series of 2-3 hour Story-sharing meetings during which each member of the Core Team shared interesting information about each participant whose transcript he/she read.

Theme Development:

UNINFORMED & OVERWHELMED - Participants lacked financial knowledge as well as the time to dedicate to learn more and improve their situation

INVITE ME TO TAKE THE NEXT STEPS - Participants were open to and would welcome help, but most often they prefer to be approached as many didn’t know where to turn for financial help (preference of channel and manner in which they should be approached differed by consumer). However, most consumers were afraid of the “hard sell” and should be approached carefully.

BUILDING & MAINTAINING TRUST - The idea of trust was very emotionally and sometimes irrationally driven. It extended beyond the institution itself and encompassed the individual providing the services. There was also a strong distrust in the stock market, fueled by a lack of understanding.

YOU HAVE THE POWER TO MAKE ME A BETTER CUSTOMER - Participants expressed a strong desire for feedback, positive reinforcement, empathy and acknowledgment. They felt that it is the bank’s responsibility to motivate their engagement and loyalty through actions, outreach and tools.

KEEP IT SIMPLE & RIGHT FOR ME - Inclusive of transactional banking, understanding reward programs and easy redemption process as well as explanations and education around lending process and long-term investing.

INSIGHT FRAMEWORK | Identifying Attributes + Relationship Drivers / Persona Development

Identifying Attributes + Relationship Drivers:

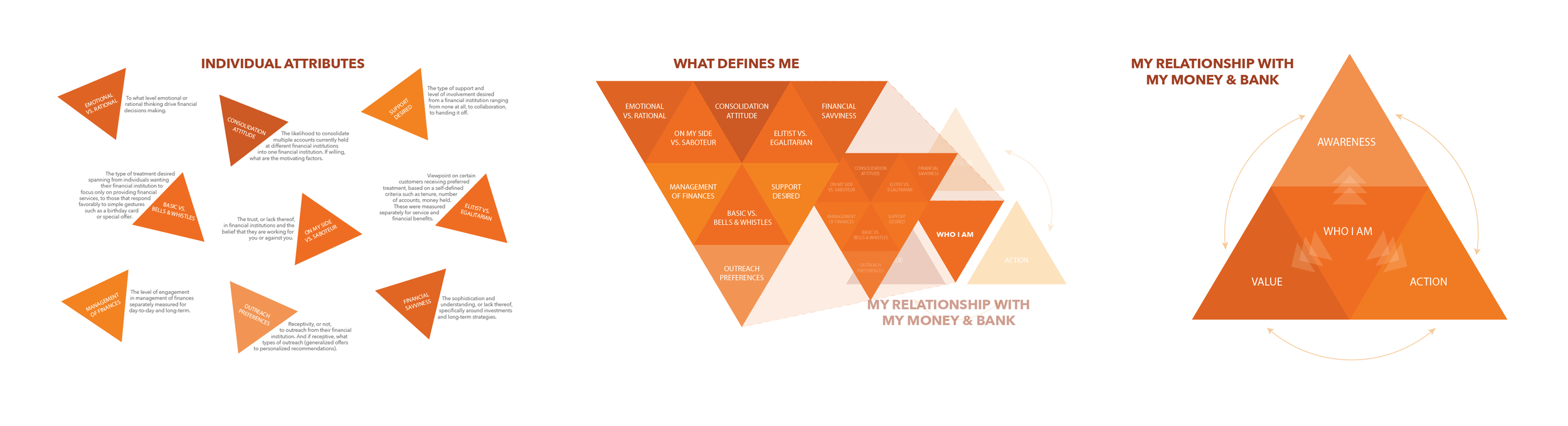

As we synthesized the data from the 42 interviews, attributes emerged that defined attitudes toward finances, motivations, actions, and preferred experiences. We narrowed it down to the nine key attribute categories listed and defined below. These individual attributes define each unique Mass Affluent consumer’s behaviors, motivations, and needs and directly impacts their relationships with their money and financial institution(s).

Emotional vs. Rational: To what level emotional or rational thinking drive financial decision making.

Basic vs. Bells & Whistles: The type of treatment desired spanning from individuals wanting their financial institution to focus only on providing financial services, to those that respond favorably to simple gestures such as a birthday card or special offer.

Management of Finances: The level of engagement in management of finances separately measured for day-to-day and long-term.

Consolidation Attitude: The likelihood to consolidate multiple accounts currently held at different financial institutions into one financial institution. If willing, what are the motivating factors.

On My Side vs. Saboteur: The trust, or lack thereof, in financial institutions and the belief that they are working for you or against you.

Outreach Preferences: Receptivity, or not, to outreach from their financial institution. And if receptive, what types of outreach (generalized offers to personalized recommendations).

Support Desired: The type of support and level of involvement desired from a financial institution ranging from none at all, to collaboration, to handing it off.

Elitist vs. Egalitarian: Viewpoint on certain customers receiving preferred treatment, based on a self-defined criteria such as tenure, number of accounts, money held. These were measured separately for service and financial benefits.

Financial Savviness: The sophistication and understanding, or lack thereof, specifically around investments and long-term strategies.

The individual attributes that define each unique consumer and his/her behaviors, motivations, and needs directly impact the relationships the consumer has with his/her money and with his/her financial institution(s). These relationship drivers can be broken down into three areas - awareness, action, and perception.

AWARENESS: Realization of an unmet financial need.

Ignorance - (blissful ignorance and acknowledgment of ignorance)

Need for knowledge - (self-discovered, externally identified)

Complacency - (awareness of need but lack of motivation to change)

Happenstance - (unsought awareness accidentally gained)

ACTION: Drivers behind an individual’s attitude and approach to money management and financial planning, as well as instances that spur a specific financial decision.

Formative experiences - (significant financial event such as a major gain or loss)

Upbringing - (parents’ financial comfort, learned financial/investment management)

Application of knowledge gained - (realization of need drives action)

Time - (perceived or true lack of time, time constraint or removal of constraint, time sensitivity)

Monetary threshold - (self-defined as the amount which is needed in order to justify making a significant step or change in your financial strategy)

Incentive - (limited time deal/offer, “toaster”)

PERCEPTION: Customer expectations for the relationship with their financial institution driven by the two-way value exchange.

“How I see myself” – Worthiness, self-determined worth relative to other customers (range: undeserving, intimidated but on the cusp, financially worthy)

“How my bank should see me” – A customer’s perceived value to the bank and resulting expectations and rules of engagement

Expanding the relationship - when relationship with the bank expands (through money, additional accounts, or the sharing of their personal information) customers expect an increase in meaningful value (through rates, customer service, fees, more thorough and informed advice).

Transparency - customers seek transparency from their financial institution in the form of being up front with fee structures and rewards, showing how the bank is profiting from monies held, and the use of customer information.

Authenticity – customers expect the bank to understand their specific situation and to use that information to make recommendations that meet understand me and use that information to meet my needs

Each person’s unique attribute makeup influences his/her financial awareness, including the baseline financial awareness a consumer has, a consumer’s receptivity to gaining new financial awareness, and the ability a consumer has to become aware of a knowledge, product, or service need. This attribute makeup also influences the consumer’s financial action. For example, the consumer’s proclivity to take action, the need threshold that must be surpassed for a consumer to take action, and the speed with which, and manner in which, a consumer takes action. Finally, the attribute mix also defines consumer perceptions, including the consumer’s perceptions of his/her value to his/her financial institution(s) and the value his/her financial institution(s) provides to him/her, the way in which the consumer views the technical value exchange between him/herself and his/her financial institution(s), and the way in which the consumer views his/her financial institution(s). These three areas that largely define the relationship a consumer has with his/her money and financial institution(s) also interact with one another. For example, a consumer gaining awareness about a financial need can spur him/her to take action to meet the need. If this need awareness came from an individual at the consumer’s primary bank, the consumer may view this information sharing as a value he/she receives from the bank and may also see his/her opening of a new product to meet the need he/she has just become aware of as a value he/she is providing to the bank. In this scenario, the value imparted from the bank to the customer led to a need awareness that spurred action and led to the customer providing value to the bank (value [bank to customer] > awareness > action > value [customer to bank]).

Persona Development:

IDEATION + PRODUCT VISION |

We hosted a series of brainstorming and co-creation sessions with internal stake holders and Mass Affluent customers. We ran each idea through a set of filtering criteria to determine best strategic fit. We developed out three concepts into working prototypes - due to the sensitivity of work, concept directions are outlined below:

Relationship Builder:

Provide experiences that are relatable, reliable, and relevant by understanding the customers’ individual attributes and how these influence their awareness, action, and perceptions

Help financial partners effectively navigate decisions/changes by taking into account short- and long-term considerations and helping them conceptualize how short-term actions affect long-term outcomes

Help solo money managers effectively plan for the present and the future

Match customers with financial advisors that can customize their guidance based on the individual’s or couple’s individual attributes

PNC Hub:

Provide customers with a secure way to view and manage all financial accounts in one place

Go beyond just an aggregation dashboard and provide valuable insights through a variety of delivery methods based on a truly holistic view of a person’s financial picture to offer real value for aggregating more account information and to demonstrate compelling reasons to consolidate accounts

Enable customers to simulate changes to their financial picture and current strategies, such as life-stage transitions, to see both short- and long-term effects of potential changes

Provide the customer with the ability to easily execute these changes (including opening/closing accounts and moving money between accounts) from one PNC dashboard

Customer can share aggregated data, goals, simulation results, and plans to lead to a deeper conversation with PNC bankers and financial advisors

Common Cents:

Provide current mass affluent families with the ability to have healthy and constructive financial conversations with their children

Education platform seeks to help the children develop financial literacy and money management capabilities, while providing their parents the opportunity to monitor their kid’s progress and learn side-by-side as needed